Allowing Hydro Lakes to Be Lowered During Dry Spells: Does the Idea Hold Water?

Image: Lake Hāwea, image credit: Rob Zohrab.

Implications on the Energy Market

Recently, we saw headlines in national news discussing applications by both Meridian Energy and Contact Energy seeking to extend the operating ranges of Lakes Pūkaki and Hāwea, respectively, by allowing them to be run down lower as-of-right, accessing so-called “contingent storage”.

The lower lake levels relating to contingent storage can currently only be accessed during extreme dry periods, to avoid the need to ask consumers to make large reductions in electricity consumption.

The rationale behind the applications is to address some of the pressure of future energy ‘crises’ and dry-year risks.

But What is the Real Benefit to New Zealand?

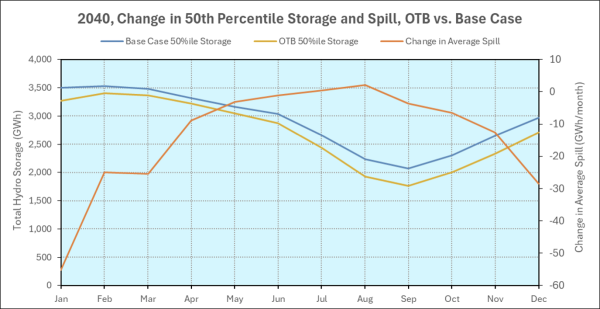

In the October edition of the Energy Link Price Path (our long-term electricity price forecast, issued each and every quarter), we included an Outside-the-box (OTB) scenario which assessed the impact on the market of allowing one of our key hydro lakes to access their contingent storage more freely.

The OTB scenario assumed Meridian Energy could routinely access an additional 350 GWh of storage in Lake Pūkaki, representing an increase of about 18% in usable storage available in this lake.

This OTB scenario was not a thorough investigation of the impact of accessing contingent storage, as we only changed the storage settings in Lake Pūkaki, and did not investigate how the rest of the market might react to this change. Nevertheless, it is a “first look” at the routine use of contingent storage which gives some useful insights, but also suggests further investigation that could be undertaken.

So, What Do the Results Show Us?

The chart shows the 50th percentile of forecast lake levels for the year 2040, for both the Price Path’s Base Case (blue curve) and the OTB scenario (yellow curve), with the OTB scenario lake levels consistently lower throughout the year than in the Base Case.

All curves are actually the average over 94 sequences of the historically recorded water inflows into Lake Pūkaki, dating back to April 1931. The lower average arises because Lake Pūkaki can be run lower in dry years, but also because it is not held as high over summer, thus reducing the amount of time it is 100% full, during which excess water has to be spilled down the Pūkaki River at the Lake Pūkaki control structure.

The chart also shows the change in average spill (orange curve) between the two scenarios, which is most prominent in the summer months, where spill is significantly less in the OTB scenario compared to the Base Case.

What Does That Mean?

Having our hydro storage lakes at a lower level on average means that when a rain event occurs, there is a greater likelihood that all of the water dumped into the catchment will be able to be held in the lake for electricity generation rather than being spilled down the river due to too-high lake levels.

It can be seen that in the summer there is a reduction in spill, to the tune of 30 - 50 GWh per month, with the difference only minor in winter, when the lakes are typically lower and therefore less prone to spill. Over the whole year, the total change in average spill is 167 GWh, which is equivalent to the annual demand for electricity at Balclutha or Whanganui.

The water that is not spilled in the OTB scenario is thus available to be used for generation at some later time, so the OTB scenarios also requires less thermal generation (gas, coal or wood-fired) than the Base Case, and hence produces less CO2 emissions than the Base Case.

How Does This Impact the Price of Electricity?

The effect of this additional storage in the long-term is to displace expensive thermal generators through the winter, reducing peak prices (a relief for those exposed to wholesale spot prices).

Once the winter is over and the lakes are refilling, hydro operators are more conservative than they are in the Base Case, in order to have the lakes filling up through spring and summer in preparation for the following winter period of high demand. This has the effect of increasing summer prices, which provides a boost to the earnings of solar farms.

As thermal generation gets more expensive into the future, the displacement of thermal generation in the winter months means that we also expect a reduction in annual average wholesale electricity prices, although the magnitude of this reduction depends on a range of factors that were not all investigated in the OTB scenario.

Prime amongst these factors is how the thermal generators might change their mode of operation in response to the overall reduction in thermal generation: but this is a topic to be investigated another day.

Find out more about our Price Path HERE.